Genre: Finance

Author: Eric G. Falkenstein

Title: The Missing Risk Premium: Why Low Volatility Investing Works (Buy the Book)

Summary

For decades, the capital asset pricing model, or CAPM, has dictated the way investors think about the relationship between return and risk. In its simplest form, CAPM states that in order to take on a risky investment, an investor must be compensated by a greater return.

This “risk premium” is a cornerstone of modern portfolio theory and is central to almost every model of asset pricing or return projection in use in the financial industry. To many investors, the principles of CAPM and its offshoots are the closest

There is a problem with CAPM, however – empirical evidence is increasingly showing that it isn’t accurate. This foundational pillar of finance, that risk-averse investors demand premiums for the risk they bear, simply isn’t true.

In The Missing Risk Premium: Why Low Volatility Investing Works, a book that may well prove to turn the investing world upside down, Eric Falkenstein explores what many have called the “low beta anomaly” – the fact

By exploring and poking holes in the theoretical basis of standard financial theory, cataloging the empirical evidence against, and sorting out the practical implications of his research, Falkenstein makes a convincing case against one of the sacred cows of investing.

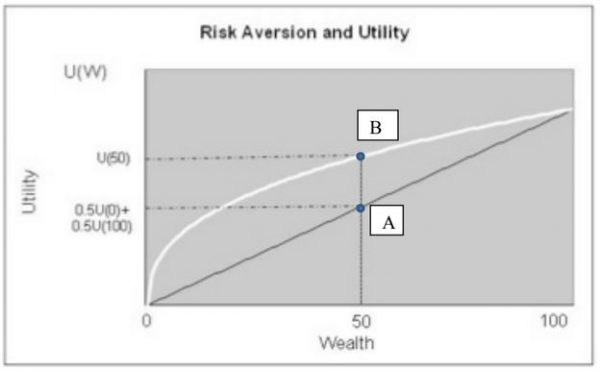

CAPM at its core applies a simple theory of risk-aversion based on the marginal utility of wealth. An extra dollar has less utility to a millionaire than to someone with nothing. The resulting convexity of the utility function explains why someone will prefer a 100% chance at $50 rather than a coin flip for $100, an aversion to risk that should carry over to the pricing of investment assets.

A rational investor should value a sure thing over a long shot, and thus accept less return for the chance to do so. Research in the

Falkenstein explores more recent evidence, however, that refutes the notion that higher risk is compensated with higher returns. In examining the correlations between return and volatility for twenty-five assets, he finds that for most a zero or sometimes even negative risk premium exists.

One study of equity returns, for instance, shows that the highest quintile of stocks in terms of volatility had the lowest returns, suggesting a negative risk premium. Similarly, on a country level, there is no correlation between a nation’s stock market return and its standard deviation.

If traditional risk premium theory held, the riskier countries would have higher returns in the long run, as investors demanded compensation for the increased risk. In practice, this simply isn’t the case.

Falkenstein explains this phenomenon of zero and negative risk premiums as a misapplication of the standard utility form. He argues that rather than constructing a utility function using wealth in absolute terms, it would be better to focus on relative wealth.

He argues that it is not greed that drives individuals, but envy. An investor’s satisfaction is more dependent on how much wealth they accumulate in comparison to some societal standard, a “benchmark,” than it is in absolute terms. With this adjustment, the theory behind the traditional risk premium fails to hold.

As a result of his findings, Falkenstein recommends low volatility investing through long-only Minimum Variance Portfolio investing. Such a strategy, he shows, can create higher returns with lower volatility, fewer transactions, and high levels of liquidity. Historical results show

First dismissed as impossible, or even crazy, Falkenstein’s theories are beginning to gain traction. Major financial institutions are setting up low volatility strategies, and the low beta anomaly is seeing increased attention in academic circles. The lesson here is, as it always is in investing, that it is never best to blindly follow the crowd. Today’s contrarian strategy is tomorrow’s conventional wisdom.

Introduction

Recent evidence that low beta stocks have outperformed high beta stocks has caused quite an uproar in financial academia. This evidence undercuts one of the foundational pillars upon which modern financial theory was built: risk-averse investors demand premiums for the risk they bear. If this evidence is true, then it would turn the financial world upside down.

While many are puzzled by this anomaly, Eric Falkenstein believes this makes perfect sense, as our current understanding of risk is misguided and the idea of risk premiums are not all they appear to be. Falkenstein explains these topics as well as some intriguing theories in his new book The Missing Risk Premium: Why Low Volatility Investing Works.

The Problem with Risk

Courage, according to many philosophers, is the hardest of all virtues to master because it requires one to risk physical or mental harm in order to achieve something great. In today’s society most courage takes its form in a mental capacity rather than a physical one.

Life doesn’t present many risk-taking opportunities to sacrifice one’s life or risk serious physical harm

In reality, most opportunities that life throws at us are the ones in which we mentally risk embarrassment from choosing something that is not normal. We have to go against the grain and deviate from what is expected. It is essentially the virtue form of risk.

Dr. Falkenstein believes risk should be treated just like courage. In fact, it should be treated just like every other virtue in life, to be used in moderation. Not too much, but not too little. Courage, as with every other virtue, is at a level of mastery when it is balanced between complete deficiency and over-excessiveness.

The optimal level of courage should fall somewhere between cautiousness and recklessness. The same goes for risk.

But that does not mean they are more likely to win the battle by being more reckless with their lives. They must have courage/risk in order to

Falkenstein argues that there should not be a linear relationship between the risk/reward function

He says that somewhere along the way, investors started twisting the phrase, “To get rich you must take

The idea that we should be rewarded for withstanding some sort of pain is absurd and not practical in other

The Rise of the Standard Model

CAPM and other pricing models based off its framework were derived from two main pillars: (1) the diminishing marginal utility of absolute wealth and (2) the statistics of portfolios. The standard model is merely a logical application of these assumptions.

The standard utility assumption implies that as wealth increases one’s utility, or satisfaction, increases at a diminishing rate

For example, a person with $1 would be more satisfied with an increase in $50 than a millionaire who receives the same $50. Mathematicians, Johnny von Neumann

This is explained in the figure below, where the average level of utility between

The second assumption is based off the Harry Markowitz’s discovery on the effects of diversification. This idea of diversification very simply states not to “put all your eggs in one basket” and is a concept that goes as far back in time as Shakespeare and the Bible.

Markowitz proved that diversifying a portfolio could eliminate all firm-specific risk, leaving only systematic risk for the investor to bear. From this idea Markowitz graphed pairs of assets on a standard deviation/return plot. This revolutionized the study of risk/return by allowing others, such as Tobin, Sharpe, Ross and Fama, a conceptual framework to build off of.

In 1962, researchers at the University of Chicago released documentation of the aggregate stock index for the period 1926-1962, a 5% return premium over the risk-free rate was noted during this period.

Not only was this a monumental moment for index reporting but, more importantly, it solidified Markowitz, Tobin, and Sharpe’s hard work on modern portfolio theory and asset pricing. It proved that stocks, which are risky, commanded a premium for that risk over the

In the early 1990’s Eugene Fama and Kenneth French published a paper that showed the significance of a size effect and ultimately disproved CAPM.

Twenty years after the creation of CAPM, the theory was finally rejected. However, the theory was not dead. “It would be naïve to think that after letting such a fundamental theory take root for a generation, any simple fact would cause the academy to simply say ‘oops!’” Fama and French presented a 3-factor model that relied upon the framework of CAPM while introducing two additional factors: size and value.

CAPM has been so deeply rooted in the foundations of financial theory, that models still use its framework today. Falkenstein explains, “Attempts to unify or generalize the model have failed repeatedly, yet the risk premium remains the centerpiece of finance, the idea that it is omnipresent and important.”

Empirical Evidence

“One can show a framework is highly improbable by showing that the undiscovered true theory the framework allows, must have some insanely improbable properties.”

In Falkenstein’s mind, the “most damning evidence” against the relationship between risk and return is the “scope of volatility-return failure across asset classes.” For this reason, he examines twenty-five assets and measures the correlation between return and volatility.

For most assets, he discovers that a zero or even sometimes a negative risk premium exists. Six of Falkenstein’s most interesting observations are summarized below.

Negative Risk Premium

Equities – In 2006, several professors from Columbia University accidentally discovered that stock variance was negatively related to cross-sectional returns. They generated the residual volatility using the Fama-French 3-factor model and found that stocks with higher volatility had lower returns. These astounding results are evident in the table below.

Some experts argue that the higher results of low-volatility returns are merely reflected in the value factor. Falkenstein believes this is unlikely because the effect of the value coefficient is not symmetric as the “highest beta stocks really suffer the greatest return fall- off.” Additionally, the higher beta stocks have greater weight on the size factor, which falsely raises expected return.

Betas-Falkenstein grouped various portfolios by their beta and created the table below. Data on common stocks from 1962 – December 2011 was attained in formulating the results. The Beta 1.0 portfolio had the greatest returns of all portfolios.

Other notables were the sharp decline in the geometric averaging of the high beta portfolio. Geometric averaging is significant in calculating returns as each year is dependent upon the past year. This technique more accurately reflects the overall change in wealth to an investor. Additionally Sharpe ratios were much higher for lower beta portfolios.

Opposition to these results comes in the form of questioning the techniques in gathering data. According to Falkenstein, “If you include all stocks, including low-priced stocks with substantial bid-ask return bias, the higher beta stocks generate inflated returns.” This mistake represents an unrealistic measurement in real life trading and helps prop up particular models.

Volatility – If the standard model (standard risk premium) holds true then people should be increasing their expected returns in volatile markets and it should manifest itself in actual returns.

However, studies that have looked at the VIX (volatility index that measures the expected movement in the S&P over the next 30-day period) compared to the one-month forward returns of the S&P 500 have found no such correlation. While volatility is not risk per se, it is linked with many of the abstract factors that modern models define as

Zero Risk Premium

World Returns – In 2006 Dimon, Marsh, and Staunton recorded returns to stock markets around the world for the years 1900-2005. They used 17 countries in their data, representing nearly 90% of the world market capitalization.

Their study focused on average equity returns; however, they came across the astonishing discovery that there was no risk-return relationship among the seventeen countries. Essentially, investors do not demand higher risk premiums for investing in more volatile countries. Similarly, the same pattern is found among emerging markets.

There seems to be no correlation between the geometric return and the standard deviation. According to Falkenstein, “The bottom line is that if you knew something about the relative volatility of various countries in the day prior to any realistic ability to move capital into other countries, it would have been useless in trying to ascertain the future relative return of that country.”

Hedge Funds – Hedge funds, while very diverse, peaked at $2.5 trillion under management in 2007 and are thus significant. If any managers had the ability to find above average returns, it would be hedge fund managers. But the ultimate question asks, after management fees and profit fees, does this amazing return trickle down to the passive investor? Falkenstein uses HFRI, which is the most popular hedge fund index, to gather data.

The HFRI produced an average return of 9.2 percent from 1990 to October 2011, 4.03 percent higher than the S&P 500 at only half the volatility. Hedge funds seem to offer above average returns at below average risk, but that information is also filled with bias.

According to Falkenstein, the short lives of successful funds (survivorship bias) and the lack of historical record reporting (backfill bias) overstates the actual returns found in hedge funds. After accounting for these biases, the return reduces by 6.6% making it lower than the S&P 500 and not providing a premium to the benchmark.

Corporate Bonds – Altman, Bana, and Kozhemiakin all noted that there is no premium to investing in corporate bonds with a 3.84% annual default rate (high-yield bonds) compared to investment grade. The Merrill Lynch High Yield index shows an 8.27% return relative to the 7.63% investment-grade return from March 1987 through December 2011.

This modest risk premium implied by the index is overstated due to the systematic bias that indices tend to have when representing illiquid asset classes. When compared using ETF’s the high yield shows a dramatic drop in return. The bottom line, says Falkenstein, is that “when one goes from BBB to C rated bonds, there is no risk premium within corporate bond returns.”

Falkenstein analyzed nineteen more assets and concluded the data on risk and returns does not seem consistent with any general risk premium story.

While he found a few assets with positive risk premiums, these were clearly the exceptions not the standard. His results can be seen in the table below:

How Does a Zero or Negative Risk Premium Make Sense?

Falkenstein explains this phenomenon of zero and negative risk premiums as a misapplication of the standard utility form.

The standard utility function used today refers to wealth in absolute terms. Falkenstein would disagree with this point, saying that individuals care more about their wealth in relative terms than in absolute terms. He argues that it is not greed that drives individuals, but envy.

An investor’s satisfaction is more dependent on how much wealth they accumulate in comparison to some societal standard, a “benchmark,” than it is in absolute terms.

The Easterlin Paradox was a common study performed by various professionals to test the level of happiness around the world.

The study showed that within a particular society, rich people are happier than poor people, but overall rich countries are not happier than poor countries. In other words, it is not the amount of money one has that makes them happy but rather the amount of money in comparison to those around them. In Japan, per capita income rose 500 percent from 1958 through 1987, yet there was little change in subjective well-being.

According to Falkenstein, “wealth does not appear to be the simple producer of happiness many thought it was.” If this is true, it has ramifications through many self-betterment economic theories and specifically the basic utility function.

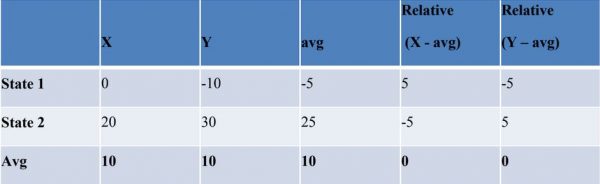

A relative utility function (envy) would be more useful in explaining risk aversion than one based on absolute terms (greed). The following model could explain a relative-oriented utility function, where one’s utility from x-wealth is equal to its utility deviation from some sort of benchmark or mean:

Falkenstein uses a simple example to explain how the new relative-oriented utility function justifies the zero and negative risk premiums.

Suppose an investor has the option between two assets X & Y with the available states. Conventionally, Y is the riskier asset because it has a higher variance than asset X, but in a relative sense, they have the same risk. The deviations of X and Y are both symmetric in that during state 1 the asset out/under-performs the average by 5 points and in state 2 the asset under/out-performs the average by 5 points.

They both have the same risk in a relative since. Risk in this example is unnecessary as you could simply put half your money in X and half in Y and average the same return with much lower risk.

Falkenstein says, “The move from looking at absolute wealth to relative wealth is important, and only the relative wealth assumption is consistent with a missing risk premium.”

Practical Implications

According to Falkenstein, “too many investors naïvely think that merely taking risk generates the payoff for such risk.” Risk is unavoidable, the key is being smart when taking risk and using it to your advantage. Falkenstein recommends low volatility investing through long-only Minimal Variance Portfolio (MVP) creation.

This strategy has been proven to create higher returns at lower volatility. Historical data has shown that this reduces volatility by 30 to 45 percent. This is in part because low volatility is not transaction heavy, does not require difficult short sales, and provides liquid investment opportunities.

Every six months Falkenstein creates MVP portfolios “using either fifty or twenty-five constituents from the various indexes.”

He then weights the portfolio based on

The MVP portfolio outperformed the index approach by 3.3 percent with 35 percent less volatility. Additionally, an investor can improve the MVP approach via a portfolio of worldwide MVP’s. This will increase diversification and mitigate any country specific risk.

Conclusion

Clearly, the evidence suggests that higher risk does not demand return premiums. Could this be an exaggerated anomaly of the system or is it really the new standard? One thing is clear, Eric Falkenstein has provided some very intriguing arguments to counter the standard understanding of risk and has his beliefs set on low-volatility investing.

After being rejected multiple times by academia and industry professionals, Falkenstein put his theory to the test and made $3.5 million since applying this theory. Whether academia or industry professionals accept these results as valid, only time will tell.

“The truth will eventually be accepted for a variety of reasons, but it takes a while.” Eric Falkenstein

Britt always taught us Titans that Wisdom is Cheap, and principal can find treasure troves of the good stuff in books. We hope only will also express their thanks to the Titans if the book review brought wisdom into their lives.

This post has been slightly edited to promote search engine accessibility.